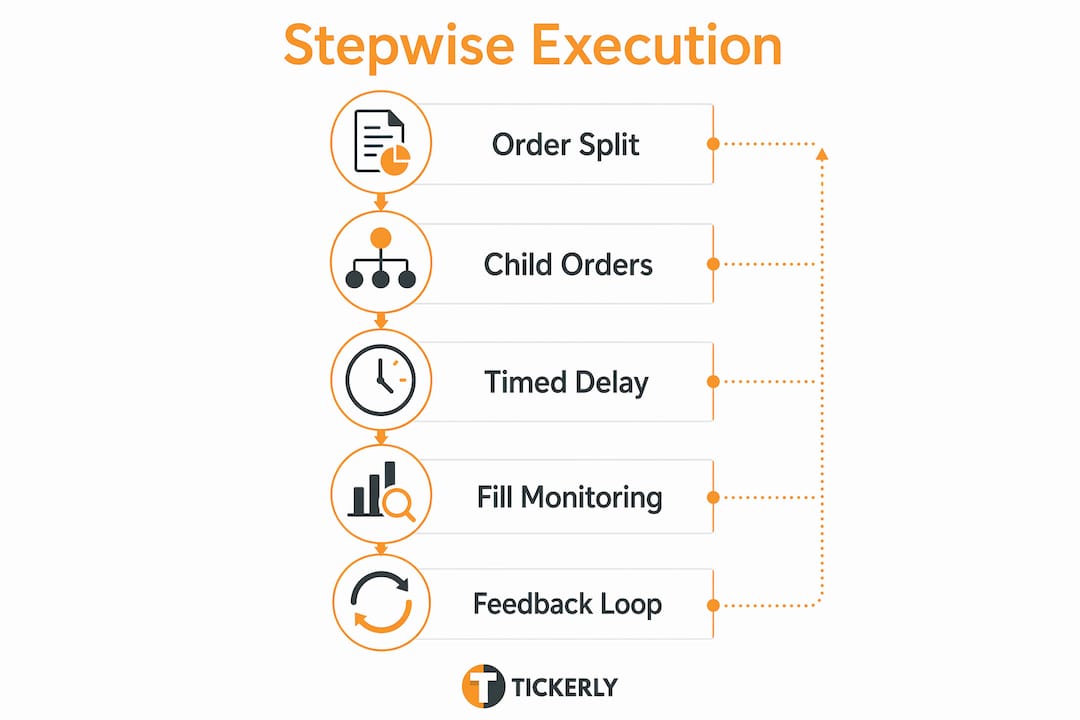

Stepwise trade execution is defined as the process of splitting a large order into multiple smaller child orders, spaced over time, to reduce market impact and improve fill quality. The industry standard term for this approach is algorithmic order slicing, and it sits at the core of professional execution desks worldwide. Rather than sending one large order that moves the market against you, you distribute volume across time, allowing the order book to recover between fills. Tools like the DARWIN MT5 splitting library and frameworks like the Almgren–Chriss optimal execution model formalize this logic into configurable, repeatable systems. For active traders and portfolio managers, mastering this process is the difference between a strategy that works in backtesting and one that holds up in live markets.

What tools and setups are required for stepwise trade execution

Effective phased trading starts with the right infrastructure. The two most common environments for implementing order slicing are MetaTrader 5 (MT5) and TradingView with an API-connected execution layer. MT5 offers native timer-based scripting, making it the preferred platform for custom splitting libraries. TradingView, paired with a webhook-to-broker bridge like Tickerly, handles the signal generation side while the execution layer manages order dispatch.

The core libraries and adapters you need include:

-

DARWIN MT5 splitting library: Handles child order creation, delay configuration, and exit management within MT5. The library spaces child orders by 10 seconds by default, with the delay configurable based on instrument liquidity.

-

SQX adapter with openPositionSplit(): Integrates with StrategyQuant X for traders who build and test strategies before deploying them live. The adapter wraps the splitting logic into a single function call.

-

Broker API with volume constraints: Any execution environment must expose VOLUME_STEP and VOLUME_MIN parameters. Improper handling of these constraints leads to systematic over or under sizing that compounds across a portfolio.

Configuration parameters that directly affect execution quality include the split count (how many child orders to create), the delay between slices (measured in seconds), and the volume rounding method. The remainder from integer division of total lots by split count should always be allocated to the first child order, not discarded. This preserves intended position size and keeps risk calculations accurate.

Hardware requirements are minimal. A VPS with low latency to your broker’s server matters more than raw processing power. Timer precision at the millisecond level is sufficient for most FX and CFD instruments, where liquidity recovery happens over seconds, not microseconds.

Additionally, you can include the logic for stepwise trade execution directly in your TradingView strategy script, allowing for more precise control over your trading entries and exits. For example, you might implement a system where a trade is only entered after confirming multiple technical signals, such as a moving average crossover combined with a breakout above a resistance level. Similarly, you can set up partial exits at predefined profit targets or stop-loss levels, and then continue to hold the remaining position, adjusting your stop-loss dynamically as the trade progresses. This approach helps in managing risk more effectively and optimizing your profit potential by executing trades in a disciplined, step-by-step manner within the script itself, rather than relying solely on manual intervention or external tools.

Pro Tip: Before deploying any splitting setup, test your volume rounding logic on a demo account with your exact broker. Different brokers enforce VOLUME_STEP differently, and a mismatch that seems trivial at 0.01 lots becomes material when you scale to 10 or 50 lots.

How does the stepwise execution process work step by step

The trade execution process follows a defined sequence from order calculation through to full position exit. Here is how each stage works in practice.

-

Calculate total lot size and split count. Divide your intended position size by the number of child orders. Assign the remainder to the first order (pos0). For example, 1.03 lots split into 10 orders gives 10 orders of 0.10 lots, with pos0 carrying 0.13 lots.

-

Send the first child order (pos0) immediately. Register its ticket number in a tracking array. This order carries your stop loss (SL) parameter. If SL is triggered on pos0, the library treats it as a signal to cancel all pending child orders.

-

Trigger subsequent child orders on a timer. Each subsequent order fires after the configured delay. The delay allows the order book to replenish between fills, which is the core mechanism that reduces order signaling and price impact.

-

Monitor stop loss and take profit independently. Each child order carries its own SL. If the market moves against you before all slices are filled, the active children close at their individual SL levels. Take profit (TP) and manual exits, however, trigger a sequential close of all remaining child orders.

-

Execute sequential exit on TP or manual close. Closing remaining child orders sequentially on a TP signal mirrors the entry logic and prevents partial position exposure. Each close fires with a short stagger (typically 1 to 2 seconds) to avoid flooding the broker’s execution queue.

-

Handle errors and retries. If a child order fails due to a requote or connectivity issue, the library should log the failure and retry after one timer cycle. Unretried failures leave your actual position smaller than intended, which distorts risk per trade.

Pro Tip: Log every ticket number, fill price, and timestamp for each child order. This data is your feedback loop. After 20 to 30 trades, you can calculate your average slippage per slice and adjust the delay interval accordingly.

What does optimal execution theory say about stepwise strategies

The Almgren–Chriss model is the foundational academic framework for understanding why and how to schedule order slices. It defines two competing costs: temporary market impact (the price displacement caused by your order, which recovers after execution) and timing risk (the cost of holding an incomplete position while the market moves). Every execution schedule is a tradeoff between these two forces.

The shape of your execution schedule is governed by the dimensionless product κT. The schedule shape governed by κT produces linear, TWAP-like execution at low values and aggressive front-loading at high values. In practical terms, a risk-averse trader who wants to minimize timing risk will front-load execution, sending larger slices early. A trader more concerned with market impact will spread execution evenly or back-load it.

| Execution Schedule Type | κT Value | Best Used When |

|---|---|---|

| TWAP (linear) | Low | Liquid instruments, low urgency |

| Front-loaded | High | High volatility, risk-averse trader |

| Concave-adjusted | Calibrated | Empirical impact data available |

The critical limitation of the classic Almgren–Chriss framework is its assumption of linear market impact. Empirical research shows that linear impact models overestimate execution costs by about 40% when actual impact is concave. Calibrating your schedule to a concave impact model reduces estimated costs by about 28%, based on backtesting across more than 3,000 VWAP orders. That is not a marginal improvement. It changes how you size splits and set delays.

“Traders should avoid relying solely on classic linear impact models for cost predictions; adapting stepwise strategies with empirical impact shapes is crucial to managing execution cost and risk.”

Emerging approaches like reinforcement learning are beginning to replace static schedules entirely. These systems observe real-time fill rates and order book depth, then adjust slice timing dynamically. For most active traders, however, a well-calibrated static schedule with concave impact assumptions outperforms a poorly tuned adaptive system.

How can traders troubleshoot and optimize their stepwise execution tactics

The most common failure mode in gradual trade execution is setting the delay interval without reference to the instrument’s actual liquidity recovery time. FX majors like EUR/USD recover within 5 to 10 seconds after a market order. Thin CFDs or small-cap equities may need 30 to 60 seconds. Using a 10-second delay on a thinly traded instrument depletes available liquidity faster than it replenishes, which defeats the purpose of splitting entirely.

Practical optimization steps include:

-

Monitor fill rates by slice. If your later child orders consistently fill at worse prices than your first, your delay is too short. Extend it by 50% and retest over 10 to 20 trades.

-

Track volume rounding errors. A systematic bias in position size, even 0.01 lots per trade, compounds across hundreds of trades. Review your remainder allocation logic if actual position size diverges from intended size.

-

Adapt exit sequences to instrument spread. On instruments with wide spreads, stagger your sequential exits by 2 to 3 seconds rather than 1 second. This prevents multiple market orders from hitting the same thin ask side simultaneously.

-

Use logs to identify retry patterns. A high retry rate on child orders signals either broker latency issues or an overly aggressive split count. Reducing split count by 20% often resolves this without meaningfully increasing impact per slice.

The balance between temporary impact and timing risk explains why there is no universal delay setting. Your configuration must reflect your instrument, your broker’s execution speed, and your risk tolerance. Treating these parameters as fixed after initial setup is the most common reason traders see degraded performance over time.

Pro Tip: Build a simple spreadsheet tracking average fill price by slice number across your last 30 trades. If fill quality degrades linearly from slice 1 to slice N, your delay is too short. If it degrades only on the last 1 to 2 slices, your split count is slightly too high for the available liquidity.

Connecting your automated trading strategies to a live feedback loop is what separates traders who improve over time from those who set parameters once and wonder why performance drifts.

Key takeaways

Stepwise trade execution reduces market impact and slippage by splitting large orders into timed child orders, with performance determined by delay calibration, volume precision, and exit sequencing.

| Point | Details |

|---|---|

| Define your split parameters precisely | Set split count and delay based on instrument liquidity, not arbitrary defaults. |

| Allocate volume remainders to pos0 | Assign rounding remainders to the first child order to preserve intended position size. |

| Calibrate for concave market impact | Linear models overestimate costs by ~40%; use empirical impact data to tune schedules. |

| Mirror entry logic in exit sequencing | Sequential exits with staggered timing prevent partial exposure and reduce exit slippage. |

| Log and iterate after every 20 to 30 trades | Fill price data by slice number is the most reliable signal for delay and split count adjustments. |

Why I think most traders underestimate the exit side of order splitting

Most of the discussion around stepwise execution focuses on entries. Traders obsess over split count, delay intervals, and impact models. The exit side gets treated as an afterthought, and that is where I see the most preventable slippage in practice.

A close-chain exit design that mirrors the entry schedule is not optional. It is the mechanism that makes the whole system coherent. Without it, a TP signal closes your first child order and leaves the remaining slices open at market, often into deteriorating conditions. I have seen traders lose 30 to 40% of their expected profit on a winning trade simply because their exit fired all orders simultaneously.

My experience with MT5 and the SQX adapter confirms that respecting symbol-specific lot steps is equally non-negotiable. A volume mismatch error at the broker level does not always throw a visible error. It silently fills at a rounded size, and you only notice the discrepancy when your account equity does not match your expected exposure. Test this explicitly before going live.

On the theory side, I would caution against overfitting your schedule to the Almgren–Chriss framework without checking whether your instrument’s impact profile is actually concave. The nonlinear impact in backtesting research is compelling, but applying it requires real fill data from your specific broker and instrument. Start with a conservative TWAP schedule, collect 50 to 100 trades of data, then adjust.

The traders who get the most out of phased execution are not the ones with the most sophisticated models. They are the ones who log everything, test incrementally, and treat their execution parameters as a living configuration rather than a one-time setup.

— Jay

Automate your stepwise execution with Tickerly

Implementing order slicing manually is time-consuming and error-prone. Tickerly turns your TradingView strategies into a fully automated trading bot, handling signal dispatch, order management, and execution timing without manual intervention.

With Tickerly, you connect your Pine Script strategy to your broker via webhook, and the bot manages the execution lifecycle from entry to exit. This removes the latency and human error that undermine manual stepwise setups. If you want to understand why automated bots improve execution quality at scale, Tickerly’s documentation covers the full workflow. For traders already using TradingView, the setup takes minutes, and the execution consistency compounds over hundreds of trades. Explore TradingView-based strategies that pair directly with automated execution for a complete system.

FAQ

What is stepwise trade execution?

Stepwise trade execution is the practice of splitting a large order into multiple smaller child orders sent at timed intervals to reduce market impact and slippage. It is also called algorithmic order slicing and is standard practice among institutional and active retail traders.

How many splits should I use for a large order?

The optimal split count depends on your total order size relative to the instrument’s average daily volume. A common starting point is slicing into 10 trades of equal size, then adjusting based on observed fill quality across slices.

What delay interval should I set between child orders?

FX majors typically recover liquidity within 5 to 10 seconds, making a 10-second delay a reasonable default. Thinner instruments like small-cap CFDs may require 30 to 60 seconds. Always calibrate based on live fill data rather than fixed assumptions.

Why does the Almgren–Chriss model matter for my execution schedule?

The Almgren–Chriss model defines the tradeoff between market impact cost and timing risk, which determines whether your schedule should be TWAP-like or front-loaded. Using it without adjusting for concave impact can overestimate execution costs by 40%, leading to overly conservative schedules.

How do I handle partial fills in a stepwise execution setup?

Log each child order’s fill price and size immediately after execution. If a child order partially fills, treat the unfilled remainder as a new order in the next timer cycle rather than abandoning it. This preserves your intended position size and keeps risk exposure consistent.