Running the same category of strategy across multiple assets isn’t diversification. It’s concentration with extra steps. Many algorithmic traders build portfolios packed with trend-following signals that look different on the surface but collapse together the moment volatility spikes. The result: drawdowns hit harder than expected, returns stagnate, and the carefully backtested edge disappears right when you need it most. This guide breaks down the exact mechanics of genuine strategy diversification, giving you a practical framework to combine uncorrelated approaches, automate execution on TradingView, and build a portfolio that performs across different market regimes.

Table of Contents

- Why diversification matters in automated trading

- How to select strategies for diversification

- Steps to combine and automate diversified strategies

- Avoiding common pitfalls: What can go wrong?

- A deeper reality: What most traders overlook about true diversification

- Automate and diversify with Tickerly’s trading solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Combine uncorrelated strategies | Mix approaches with low return correlation to lower risk and boost performance. |

| Diversify across assets and styles | Use strategies on different assets, markets, and timeframes for real diversification. |

| Monitor and rebalance portfolios | Regularly check correlations and rebalance to maintain automated portfolio strength. |

| Beware stress-period correlation spikes | Review how strategies perform in market crises to guard against hidden risks. |

Why diversification matters in automated trading

True diversification in algorithmic trading isn’t about loading up on more indicators or trading more symbols. The goal is to combine strategies that respond to different market forces so that when one approach struggles, another compensates. This is fundamentally different from simply adding more strategies to your portfolio.

The math is compelling. Strategies built on different information domains, such as regime detection, cross-asset signals, volatility term structure, and market breadth, behave independently in a way that reduces portfolio-level risk without requiring you to sacrifice return potential. Research on combining four uncorrelated strategies showed an equal-weight portfolio improved risk-adjusted returns by 28% over the individual strategy average while maintaining near-zero daily return correlation between components.

| Portfolio type | Risk-adjusted return | Volatility | Drawdown depth |

|---|---|---|---|

| Single trending strategy | Baseline | High | Deep |

| Four correlated strategies | Minimal gain | High | Deep |

| Four uncorrelated strategies | +28% improvement | Low | Shallow |

Correlated strategies fail together. If two strategies both rely on momentum and price breakouts, a sudden market reversal hits both simultaneously. You experience the drawdown of each position at the same time. That’s not diversification; that’s doubled exposure wearing a disguise.

Key benefits of genuine strategy diversification include:

- Reduced simultaneous drawdowns across the portfolio when a single market regime shifts

- Smoother equity curves that are more psychologically manageable and operationally stable

- Exposure to more return streams, particularly useful when one asset class enters a low-volatility or range-bound phase

- Greater resilience in turbulent markets where uncorrelated signals generate returns independently

Consider multi-strategy automation as the delivery mechanism. Without automation, maintaining five different strategies across multiple timeframes and assets would require constant manual oversight. Automation enforces discipline, removes emotional interference, and executes each strategy exactly as designed. You can also explore hedge mode strategies as a specific structural approach to holding simultaneous long and short positions that benefit from opposing market moves.

The payoff is real: when you optimize trading for long-term gains, diversification becomes the structural foundation rather than an afterthought. With the case for diversification established, let’s look at how to lay the right groundwork before mixing strategies.

How to select strategies for diversification

Knowing you need uncorrelated strategies is the easy part. Knowing how to identify them requires a systematic, evidence-based process.

The single most useful metric is the correlation coefficient of daily returns between any two strategies. Selecting strategies with correlation below 0.3 across assets, timeframes, and styles is the standard benchmark for building genuinely independent strategy portfolios. A coefficient above 0.5 generally means those two strategies share significant risk exposure, and combining them provides far less protection than expected.

Here’s a practical comparison of common strategy types and their typical correlation behavior:

| Strategy type | Typical correlation to trend | Best pairing candidate |

|---|---|---|

| Trend following (moving average) | 1.0 (self) | Mean reversion |

| Mean reversion (RSI, Bollinger) | Low to moderate | Trend following |

| Volatility breakout | Moderate | Pairs trading |

| Pairs trading | Low | Volatility breakout |

| Breadth/macro momentum | Near zero | Most other types |

You should also use correlation analysis on daily returns to avoid redundancy, aiming for coverage across forex, indices, and commodities and spanning multiple trading sessions across the trading week. This prevents you from building a portfolio that technically contains different strategies but all perform poorly on the same market days.

Follow these steps to build your strategy selection shortlist:

- List candidate strategies across the main style categories: trend following, mean reversion, breakout, pairs trading, and volatility trading.

- Run correlation analysis on the daily return series of each strategy using historical backtest data. TradingView’s Pine Script makes this accessible for most traders.

- Score each pair using a composite score that weights correlation coefficient, asset class coverage, and style diversity.

- Eliminate high-correlation candidates before committing to a combination. If two strategies score above 0.4 in correlation, replace one with a strategy from a different information domain.

- Test cross-asset factor momentum as an additional layer. Cross-asset factor momentum research shows that combining signals from different asset classes captures return streams that single-asset portfolios completely miss.

Pro Tip: Before you spend time correlating complex strategies, check whether two strategies trade at the same time of day on the same instruments. Temporal and asset overlap is often enough to create hidden correlation even between strategies that look structurally different.

When exploring strategy ideas for your portfolio, prioritize approaches that operate on distinct market mechanics. For example, a CCI-based regime strategy captures cyclical market phases while a volatility term structure strategy profits from changes in implied versus realized volatility. These two approaches rarely generate signals at the same time, which is exactly what you want.

If you’re focused on crypto, BTCUSD TradingView use cases offer a practical entry point into diversifying across crypto-specific signals that behave differently from traditional equity strategies. Once you understand what makes two strategies independent, the next step is testing and assembling them into a robust portfolio.

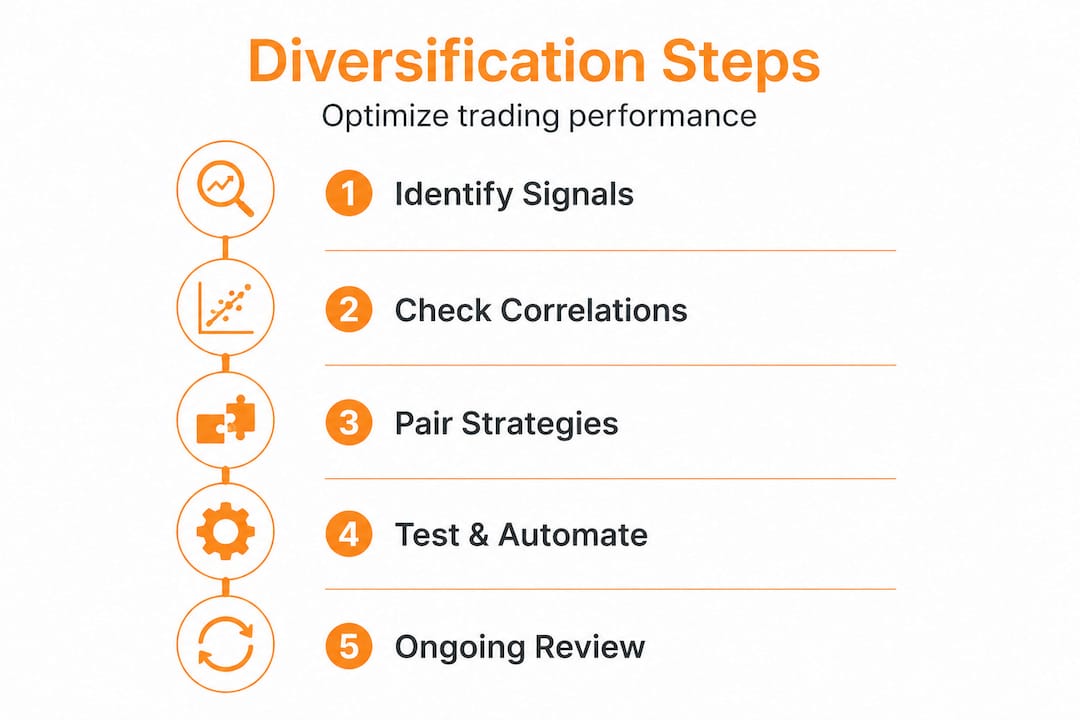

Steps to combine and automate diversified strategies

You’ve selected your strategies. Here’s exactly how to put them to work together in a resilient automation framework. The process is sequential and each step builds on the previous one.

-

Run a formal correlation analysis on backtest equity curves and daily return series for all selected strategies. Document your correlation matrix before committing to any allocation. Use TradingView’s Pine Script or export data to Excel for this step.

-

Backtest each strategy independently across at least two to three years of data, including at least one period of market stress. This is your baseline. If a strategy performs poorly alone, it won’t save a portfolio.

-

Allocate weights using either equal weighting or volatility-scaled weighting. Measuring daily return correlations and applying equal-weight or volatility-scaled allocation are both valid starting points. Volatility scaling reduces the weight of higher-risk strategies so no single component dominates portfolio variance.

-

Set up automation via TradingView alerts connected to your execution layer. Learn how to automate strategies in TradingView to trigger order execution without manual intervention. Automation ensures that your strategy weights and execution rules are followed precisely regardless of market conditions or your availability.

-

Monitor daily return correlations weekly. Markets evolve. Correlations that measured 0.2 in a trending market can move to 0.6 during a stress event. Build a weekly review into your workflow to catch this early.

-

Rebalance quarterly or whenever strategy performance or correlation patterns shift meaningfully. The portfolio automation guide supports quarterly rebalancing as the right frequency for most multi-strategy portfolios, balancing responsiveness with transaction cost efficiency.

Statistic to remember: A four-strategy equal-weight portfolio combining independent information domains delivered a 29% reduction in portfolio volatility compared to single-strategy execution. That’s a substantial reduction in risk without eliminating return potential.

Pro Tip: Build a simple performance dashboard that shows each strategy’s current contribution to portfolio returns, its rolling 30-day correlation to the others, and its current position size. Review this weekly, not just quarterly. Detecting a correlation spike early gives you time to reduce allocation before the drawdown hits.

Key automation rules to encode directly into your Pine Script or bot configuration:

- Maximum position size per strategy to prevent any single signal from dominating the portfolio

- Automatic alert pause if a strategy’s rolling correlation to another exceeds your threshold (typically 0.5)

- Daily loss limits that apply to the composite portfolio, not just individual strategies

Avoiding common pitfalls: What can go wrong?

Even well-designed diversified portfolios can underperform when traders overlook structural vulnerabilities. Understanding these failure modes before they hit you is the practical edge.

The most dangerous pitfall is assuming that historical correlations stay stable. In stress environments like March 2020, virtually all assets dropped simultaneously as correlations surged across stocks, bonds, commodities, and crypto. Strategies that appeared uncorrelated in normal markets suddenly moved in lockstep. This is not a rare edge case. It happens in every major market dislocation.

Common mistakes that undermine diversification:

- Hidden signal overlap: Two strategies relying on RSI and MACD respectively might look different but both respond to the same price momentum shifts, creating disguised correlation.

- Same asset class, different timeframes: A 15-minute trend strategy and a 4-hour trend strategy on the same instrument share far more risk than their timeframe difference suggests.

- Over-relying on stocks-bonds hedging: Cross-asset research shows that in high-inflation and rate-shock environments, stocks and bonds can move in the same direction, eliminating the traditional hedge.

- Hindsight bias in backtesting: Optimizing strategies on in-sample data and never testing out-of-sample creates strategies that appear to diversify well historically but fail on live data.

“Diversify by risk drivers, not tickers. Include true hedges like bonds, gold, and volatility products to maintain protection when standard correlations break down.”

Strategies explicitly built to profit from volatility, such as those trading VIX-linked instruments or options premium collection, behave differently from directional equity or crypto strategies. Adding stock diversification tips through automation helps you structure these exposures systematically rather than guessing.

Pro Tip: Simulate your composite portfolio through historical crash scenarios including 2008, 2020, and the 2022 rate shock. If all strategies draw down simultaneously in these scenarios, you haven’t achieved true diversification regardless of what the normal-period correlation matrix shows.

Understanding what can go wrong means you can design, monitor, and adjust your diversified trading plan for maximum resilience. When exploring risk driver diversification, focus on identifying the underlying economic force each strategy profits from and ensure those forces are genuinely independent.

A deeper reality: What most traders overlook about true diversification

Most guides on diversification fixate on asset count. Add more symbols, trade more markets, include more indicators. But that framing misses the actual mechanism. The real edge in diversification comes from combining distinct risk drivers and trading regimes, not from multiplying positions.

A portfolio holding 10 trend-following strategies across 10 different assets is far less diversified than a portfolio holding four strategies that each profit from a different market force. One regime-based strategy profits during trending conditions. A mean-reversion approach thrives in range-bound markets. A volatility strategy generates returns during uncertainty spikes. A macro breadth strategy captures broad participation shifts. Each strategy is doing something fundamentally different, and their returns are structurally independent.

The uncomfortable truth is that correlation measured during stable periods is essentially useless as a protection guarantee. It tells you how independent the strategies were when nothing was breaking. What you actually need to know is how they behave when markets break. Testing composite portfolio behavior during stress scenarios isn’t optional; it’s the central verification step that most traders skip entirely because it requires more effort and often produces uncomfortable results.

Dynamic allocation matters as much as initial construction. Markets move through regimes: trending, mean-reverting, high-volatility, low-volatility. A fixed allocation that worked well in 2023’s trending environment may be poorly calibrated for a choppy 2025 market. Continuous monitoring and willingness to adjust weights based on current regime signals is what separates a robust portfolio from one that just looks robust on paper.

From our experience working with traders using multi-strategy approaches, the biggest mistake isn’t a technical error. It’s falling in love with a strategy that’s currently working and over-weighting it at exactly the moment when its edge is about to fade. Automation helps enforce rules that prevent this emotional over-allocation, but human oversight is still the final safeguard. No bot should run indefinitely without a periodic review of whether its underlying logic still applies to current market conditions.

True diversification is a dynamic practice. Build it carefully, test it honestly, automate it systematically, and review it consistently.

Automate and diversify with Tickerly’s trading solutions

Understanding diversification principles is a strong starting point. Putting them into motion across live markets is where automation becomes essential. Tickerly turns your TradingView strategies into a fully automated trading bot, making it practical to manage multi-strategy portfolios without manual intervention on every signal.

With Tickerly, you can connect multiple Pine Script strategies to live execution, enforce position sizing rules across your entire portfolio, and monitor each strategy’s contribution in real time. Whether you’re building a four-strategy uncorrelated portfolio or scaling a single approach across asset classes, the tools are ready. See all available strategies to find combinations that fit your risk profile, or go directly to implement automation on TradingView and start running your diversified system without delay.

Frequently asked questions

What is the best number of strategies to diversify?

Aim for 4 to 6 uncorrelated strategies allocated across assets, styles, and timeframes. Research confirms strategies below correlation 0.3 across trend following, mean reversion, breakout, pairs trading, and volatility trading form effective multi-strategy portfolios.

How often should I rebalance a diversified strategy portfolio?

Rebalance quarterly or whenever correlations or performance patterns change significantly. Evidence shows that an equal-weight portfolio with periodic rebalancing improved risk-adjusted returns by 28% over individual strategy averages.

What tools can I use to test correlations between trading strategies?

Use daily return correlation analysis available in TradingView, Excel, or Pine Script tools built for this purpose. Measuring daily return correlations with equal-weight or volatility-scaled allocation methods are both accessible starting points.

Does diversification always work in market crashes?

No. Correlations increase in stress events like March 2020 when virtually all assets dropped together. Including true hedges such as volatility products, gold, and bonds helps preserve protection when standard correlations break down.

Is portfolio performance better with asset or strategy diversification?

Combining distinct trading strategies by style, asset class, or risk driver consistently outperforms simply holding more tickers. Cross-asset portfolio research confirms that mean-variance-weighted multi-asset portfolios beat equal-weight single-market allocations for most automated trading goals.