Most traders assume algorithmic trading is a product of the 2000s tech boom. That assumption is wrong, and it matters. Automated trading began in the early 1970s with NYSE’s Designated Order Turnaround (DOT) system, upgraded to SuperDOT in 1984, enabling electronic routing of orders to trading posts. Every trading bot, every Pine Script strategy, every latency arbitrage system you use today rests on a foundation built over five decades. Understanding that history is not nostalgia. It is the clearest map you have for anticipating where market structure goes next.

Table of Contents

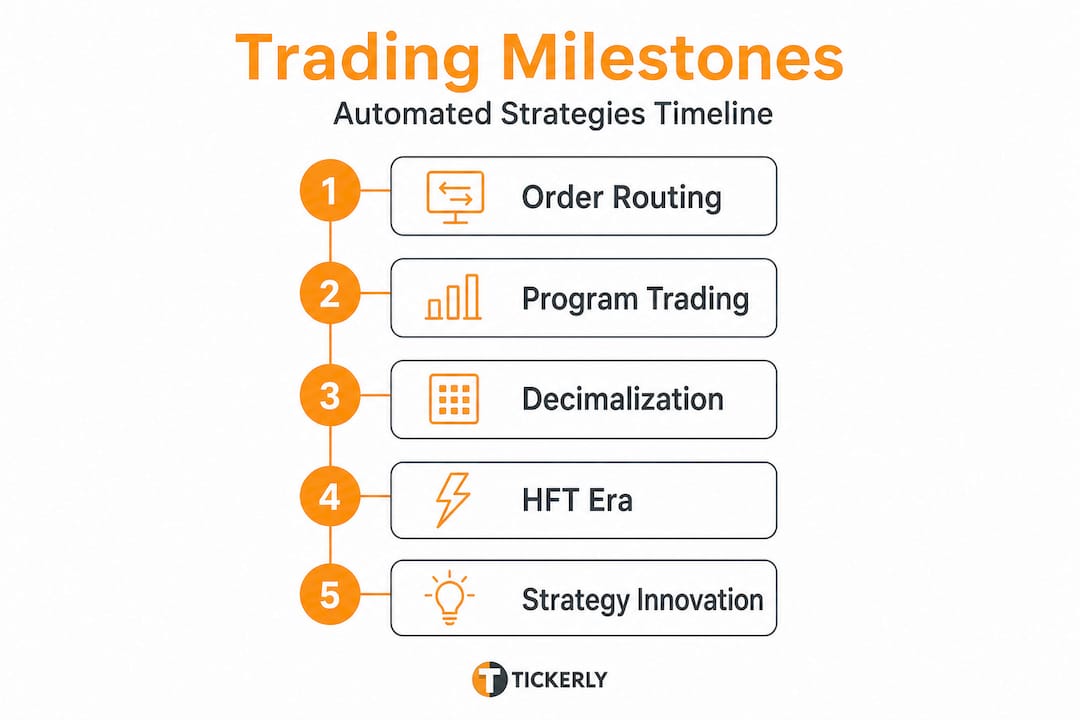

- Early origins: Mechanized order routing and initial automation

- The rise of program trading and market structure changes

- Strategic innovation: Key methodologies in automated trading

- The HFT era: Opportunities, risks, and regulation

- What most traders get wrong about automation in the markets

- Ready to apply the lessons of trading automation?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Automation began early | Automated trading has roots in the 1970s, not just recent decades. |

| Program trading changed markets | Large-scale, pre-programmed basket orders in the 1980s shaped market structure and volatility. |

| Decimalization drove HFT | Reducing tick sizes in 2001 increased liquidity and sparked high-frequency trading methods. |

| Diverse strategies dominate | Modern automated trading relies on execution algorithms, market making, and both statistical and momentum strategies. |

| Regulation balances risk | Rules and safeguards like kill switches help ensure fast markets remain stable and fair. |

Early origins: Mechanized order routing and initial automation

The story of automated trading does not begin with a hedge fund quant writing Python code. It begins with a physical problem: how do you route an order from a broker’s desk to a trading floor post without a human runner dropping the ticket? NYSE’s DOT system in the early 1970s solved exactly that. It mechanized order routing, cutting the physical delay between order entry and floor delivery.

By 1984, SuperDOT expanded on that concept, handling larger order volumes and accelerating execution. But here is the critical distinction most traders miss: DOT and SuperDOT mechanized routing, not execution. A floor specialist still matched buyers and sellers manually. True automation required electronic matching, which did not arrive until Instinet in 1969 and, more broadly, the rise of Electronic Communication Networks (ECNs) through the 1990s.

| System | Year | Function | Limitation |

|---|---|---|---|

| DOT | Early 1970s | Automated order routing | Floor-based execution |

| SuperDOT | 1984 | Higher-volume routing | Still manual matching |

| Instinet | 1969 | Electronic order matching | Institutional only |

| ECNs | 1990s | Open electronic matching | Fragmented liquidity |

Instinet was remarkable because it let institutional traders match orders directly with each other, bypassing exchange floors entirely. That was genuinely disruptive. ECNs later democratized the model, fragmenting liquidity across venues but dramatically increasing execution speed and reducing costs for participants willing to adapt.

The factors driving early automation were straightforward: efficiency, error reduction, and scale. Manual routing introduced latency and human error at every step. Automation eliminated both. If you run automated forex trading systems today, the logic your bot uses to route orders through specific venues traces directly back to the routing architectures pioneered in these early systems.

“Understanding legacy systems is not academic exercise. The market microstructures built in the 1970s and 1980s define the rules, latency profiles, and matching logic that your algorithms operate within right now.”

Pro Tip: Study the automated trading exchanges your strategy operates on. Each exchange’s matching engine has specific latency characteristics and order types that often reflect the architecture inherited from these foundational systems.

The rise of program trading and market structure changes

Once order routing became semi-automatic, trading strategies evolved rapidly. The 1980s introduced program trading, a concept that reshaped how institutional players thought about executing large positions. Program trading emerged for index arbitrage between S&P 500 equities and futures, using pre-programmed instructions to execute large basket orders simultaneously across dozens of securities.

The logic was compelling: if the S&P 500 futures price diverged from the underlying basket of stocks, an automated system could buy the underpriced instrument and sell the overpriced one faster than any human could react. The profit window was tight, measured in seconds. Only automation could reliably capture it.

This created a cascade of consequences for market structure:

- Volatility spikes became more sudden and synchronized, because dozens of basket orders hitting the market simultaneously could amplify price moves rather than absorb them.

- Liquidity patterns shifted, with automated systems providing it in normal conditions but withdrawing quickly during stress events.

- Regulatory scrutiny increased after the 1987 Black Monday crash, where program trading was cited as an accelerant to a 22% single-day decline.

- Technology investment surged as firms realized that marginal improvements in execution speed directly translated into arbitrage profitability.

The next structural shift arrived in 2001 with decimalization. Before this change, stocks traded in fractions, with the minimum tick size at 1/16 of a dollar ($0.0625). Decimalization reduced tick size to $0.01, narrowing spreads, reducing traditional market-maker advantages, and increasing overall liquidity. It was a regulatory change that accidentally turbocharged high-frequency trading.

| Market characteristic | Pre-decimalization | Post-decimalization |

|---|---|---|

| Minimum tick size | $0.0625 (1/16) | $0.01 |

| Typical bid-ask spread | Wide | Narrow |

| Market-maker profit per trade | High | Low |

| Trade volume needed to profit | Lower | Much higher |

| HFT viability | Limited | Highly viable |

Narrower spreads meant traditional market makers could no longer earn comfortable margins on each transaction. To stay profitable, you needed to trade far more frequently. That requirement eliminated manual traders and created the conditions for automated stock trading systems to dominate market-making roles. The innovation sequence here is instructive: each change in market structure created pressure that incentivized the next wave of automation.

Strategic innovation: Key methodologies in automated trading

As market structure shifted, new algorithmic strategies and optimization techniques quickly followed. Modern automated trading is not a single approach. It is a layered toolkit of methodologies, each suited to specific market conditions and asset classes. Key methodologies include execution algorithms such as VWAP, TWAP, and iceberg orders, market making with risk buffers via Hamilton-Jacobi-Bellman (HJB) equations, statistical arbitrage, latency arbitrage, and momentum or mean reversion strategies supported by backtesting.

Here is what each approach actually does in practice:

- VWAP (Volume-Weighted Average Price): Breaks a large order into smaller slices timed to match market volume distribution throughout the day. Reduces market impact by avoiding large single-execution orders that would move the price against you.

- TWAP (Time-Weighted Average Price): Spreads order execution evenly across a set time window. Simpler than VWAP but effective when volume patterns are unpredictable.

- Iceberg orders: Displays only a fraction of the total order size to the market. Prevents other participants from front-running a large position by hiding true intent.

- Market making: Simultaneously quotes both buy and sell prices, profiting from the spread. Risk buffers calculated via HJB equations help the system manage inventory exposure dynamically.

- Statistical arbitrage: Identifies historically correlated instruments and trades when their price relationship deviates beyond a statistical threshold, betting on reversion to the mean.

- Latency arbitrage: Exploits the speed difference between data feeds or venues to act on price discrepancies before slower participants can react.

- Momentum strategies: Enter positions in the direction of recent price movement, assuming that short-term trends continue.

- Mean reversion: Bets that prices will return to historical averages after overshooting in either direction.

Understanding how data powers algorithmic strategies is essential before choosing between these approaches. Each methodology makes different assumptions about market behavior, and those assumptions must be validated through rigorous backtesting against real historical data.

| Strategy type | Core assumption | Best market condition | Key risk |

|---|---|---|---|

| VWAP/TWAP | Minimize market impact | High liquidity | Slippage in thin markets |

| Market making | Capture spread consistently | Low volatility | Inventory accumulation |

| Statistical arbitrage | Mean reversion of correlations | Range-bound pairs | Correlation breakdown |

| Momentum | Trends persist short-term | Trending markets | Sudden reversals |

| Latency arbitrage | Speed edge is sustainable | Any, with co-location | Regulatory changes |

Algotrading on TradingView gives you practical access to most of these strategy types through Pine Script, making it possible to build, test, and deploy them without writing low-level infrastructure code. Reviewing algorithmic strategy types in depth before you commit capital to any of these approaches is time well spent.

Pro Tip: The best strategy is not the most sophisticated one. It is the one that matches your asset’s microstructure. A momentum strategy built for crypto will behave very differently applied to equities due to differences in market hours, liquidity depth, and volatility profiles. Always test within the specific context you plan to trade.

The HFT era: Opportunities, risks, and regulation

With strategies growing in speed and complexity, the age of high-frequency trading raised new market challenges and demanded new safeguards. HFT is not simply “fast trading.” It is a distinct operational category defined by co-located servers, proprietary data feeds, ultra-low latency execution in microseconds, and extremely high order-to-trade ratios.

The benefits are real. HFT firms acting as market makers continuously provide two-sided quotes, which tightens spreads and improves price discovery for all participants. In normal conditions, this genuinely helps retail and institutional traders get better fill prices. Liquidity is deeper and more consistent than it was in the manual trading era.

The risks are equally real and less frequently acknowledged:

- Flash crashes occur when HFT systems simultaneously withdraw liquidity during stress events, creating near-instantaneous price collapses. The May 2010 Flash Crash saw the Dow Jones drop nearly 1,000 points in minutes before recovering.

- Systemic risk increases when many firms run similar strategies, creating correlated behavior at speed that regulators and exchanges cannot easily monitor in real time.

- Arms race dynamics push firms to spend enormous resources on marginal speed advantages that add no genuine economic value to markets.

- Quote stuffing allows bad actors to flood markets with orders and cancellations, degrading infrastructure and obscuring true prices from competitors.

“HFT and automated trading are not inherently destabilizing. They become dangerous when speed advantages substitute for genuine market analysis, and when regulatory frameworks fail to keep pace with technological change.”

Contrasting views on HFT consistently show that the technology provides liquidity but risks systemic instability, and that effective regulation must balance innovation with controls like kill switches. Kill switches, circuit breakers, and order cancellation throttles are now standard tools across major exchanges globally, designed to interrupt runaway algorithmic behavior before it cascades.

For traders building automated systems, understanding long-term trading optimization means recognizing that regulatory changes in HFT directly affect your strategy’s operating environment. What is permissible and profitable today can shift quickly when regulators respond to the next market event. The interaction between banking efficiency and compliance trends and trading technology continues to define the boundaries within which all automated systems operate.

What most traders get wrong about automation in the markets

Here is a perspective you rarely encounter in trading forums or strategy guides: most traders treat the history of automated trading as irrelevant to their current systems. That is a mistake that costs them real money and genuine edge.

The assumption is that today’s markets are so technologically distant from DOT routing or 1980s program trading that those systems have nothing to teach modern algorithmic traders. But that reasoning is backwards. The behaviors baked into current market microstructure, the latency profiles of matching engines, the circuit breaker thresholds, the order type rules, and the fragmentation of liquidity across venues are all direct products of decisions made during those earlier phases of automation. You are not trading in a clean, freshly designed system. You are trading in one that has been patched, extended, and regulated in response to fifty years of crises and innovations.

Consider decimalization. That single regulatory change, aimed at fairness for retail investors, accidentally created the structural conditions that made HFT not just viable but necessary for market-making profitability. No one intended that outcome. It emerged from the interaction between technology and market structure. The same dynamic will play out repeatedly. Regulatory changes around crypto market structure, AI-driven trading transparency rules, and latency equity proposals are all in progress right now. Understanding how past structural shifts generated unintended consequences gives you an analytical framework for anticipating the next ones.

The second error traders make is treating automation as a static technology rather than a co-evolving system. Regulations and trading technology do not develop independently. They respond to each other in a cycle. Every major market disruption (1987, the dot-com era, 2010 Flash Crash, March 2020) produced regulatory responses that reshaped the environment for automated strategies. If you study our trading automation FAQ, you will find that even basic questions about order types and execution reflect design decisions made in direct response to past automation-related market events.

Pro Tip: When a major market disruption occurs, do not just analyze the price action. Study the regulatory response that follows. That response will define the constraints and opportunities for your automated strategies in the next market cycle.

Studying old disruptions to spot the next market shift early is not a theoretical exercise. It is practical edge. The traders who understood how decimalization would affect spread economics positioned themselves advantageously for the HFT era. The traders who understand how current AI transparency proposals might affect execution algorithms will have similar advantages in the years ahead.

Ready to apply the lessons of trading automation?

The history of automated trading is not background reading. It is directly applicable intelligence for building more resilient, better-informed trading systems today.

At Tickerly, we turn your TradingView strategies into fully automated trading bots, connecting decades of market structure evolution to modern execution. Whether you want to explore top TradingView strategies that have stood up to real market conditions, review the automated trading FAQ to sharpen your understanding of how these systems work, or get started directly with our trading bot platform, we have the tools and resources to move you from strategy to live execution with confidence.

Frequently asked questions

When did automated trading first start in financial markets?

Automated trading started in the early 1970s with NYSE’s Designated Order Turnaround (DOT) system and gained significant momentum through the 1980s with SuperDOT and the growth of ECNs.

How did decimalization affect automated trading strategies?

Decimalization in 2001 reduced the minimum tick size from 1/16 to $0.01, narrowing spreads, cutting traditional market-maker profit margins, and directly fueling the rise of high-frequency trading strategies that depended on volume and speed rather than wide spreads.

What are the main types of automated trading strategies used today?

Key methodologies include VWAP and TWAP execution algorithms, iceberg orders, market making, statistical arbitrage, latency arbitrage, and momentum or mean reversion systems, each validated through backtesting before live deployment.

Does high-frequency trading help or hurt markets?

HFT provides liquidity and improves price discovery in normal conditions, but it can amplify volatility during stress events, which is why regulators have implemented kill switches, circuit breakers, and order throttling rules to contain systemic risk.